In a previous life at CGI / BJSS I stood-up the Enterprise Sustainability effort, along with running and supporting the Working and Steering groups, building out the capability to get things to a point of organisation and understanding to start meaningfully driving towards Net Zero. In my current work post that organisation I’ve taken both a large and medium sized business down the same path. Through this journey I know from the hard-won experience that building a Scope 3 Emissions calculation model is hard work and it’s all based on data. Defining a data capture, refinement and reporting regimen, and learning how to identify, capture and translate that data, along with engaging people around the business who are the gatekeepers to the relevant data and business information you need are all non-trivial tasks.

What I’ve realised, in doing it myself several times and in talking with others on the Net Zero journey is the number one mistake you’re likely making is that you’re NOT thinking of accounting for your emissions data in the same way you think about accounting for your financial data. It’s almost treated as an aside to the ‘real’ work of decarbonising your organisation’s footprint. That’s the reason you’re not committing the same level of people, time, money and processes to your Scope 3 based decarbonisation goals. It’s why you’re not getting the results you want and why you’ll not achieve anything close to Net Zero in the timeframe you’re planning for it. The shift in mindset starts with a realisation that within your business money is everywhere and carbon is everywhere too – they are inseparable, they need accounting for.

…the number one mistake you’re likely making is that you’re not thinking of carbon accounting in the same way you think about financial accounting.

You know it isn’t possible to do anything in your business without incurring a financial cost. In the same way doing those same things will incur a carbon cost. For every £1 you spend you also incur a certain amount of CO2. Every time. That’s why you need to introduce carbon accounting practices from the very start of your Net Zero Journey.

Applicable accounting practice?

You would never be lax about your financial accounting and would want to apply a robust, accepted set of principles that brings confidence to those reading your financial accounts and reports. Your inhouse chartered accountant or perhaps your AAT qualified accounts team would all be applying accepted, recognised practices in a consistent way.

All the same thinking and principles apply to carbon accounting. Models like GAAP provide a translatable set of principles that makes it unnecessary for those expensive big four consultancies to reinvent the accounting wheel while you’re being billed for the pleasure of it. Though I will conceded you need a dedicated team of competent, business aware professionals with a passion for carbon accounting, just like you do for financial accounting. You’ll also need some form of accounting software, that could be a clever Excel workbook, but I have something better we can talk about so get in touch.

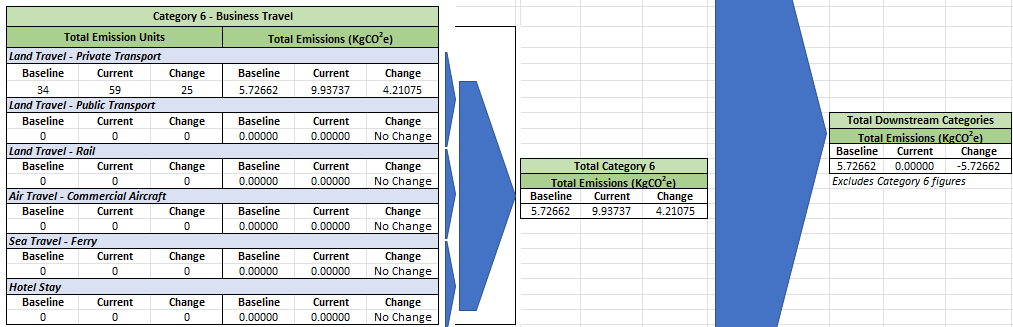

Data Translation

Let’s talk briefly about how you might go about translating the monetary value of goods and services covered by your scope 3 activities into CO2e. The GHG protocol gives us four ways of doing calculations: Supplier-specific, Spend-Based, Average-Data or Hybrid methods and you are expected to report the methods(s) used and why. The most likely readily available data is spend-based. You bought good and services of a specific type and it cost you a certain amount of money. Your accounts or procurement team should have this data (if not we need to do a little FRA as part of the Net Zero journey).

Once you have the “5 reams of paper for £20” type spend data you’ll need a way of converting that into emissions data. If the supplier has the cradle-to-gate emissions data then you’re all set and can use Supplier-specific data. It’s likely they won’t. That’s where the various data sets and sources I use come into play, particularly for the accounting categories of transport and waste. These are based on publications from trusted authorities, manufacturers and producers – think of them like your FX conversion tables. As you’ll have already deduced, you’ll almost always end up using a hybrid approach once you’re past the first few build-outs of your carbon accounting records.

Feed that data back into your accounts software and the process of data capture, translation, analysis and reporting becomes a lot easier. Alternatively, imagine you’re NOT doing it like this. Exactly, hardly a tenable approach. So next time you’re pondering emissions data – think carbon accounting.

Mark.