In our last article introducing our Carbon Accounting Platform (Veridia Carbon) we have been building we mentioned the platform was “… a Carbon Ledger, Emissions Activity Tracker and Reporting Tool rolled into one.”

Prefer to chat than read? Book a free 30 minute call and let’s discuss how we can help.

That seemed a fairly succinct description but the question raised by several connections was what exactly is Carbon Accounting? It’s a fair question, a bit like asking what exactly is Financial Accounting. Indeed the follow on was if it was anything like that. The answer is “yes, but no”. Let’s look at the fundamentals then, because if we’re not sure what it is how can we be sure we need it.

What actually is Carbon Accounting? It’s a fair question.

Greenhouse Gas Accounting

Many of you will have heard of the Greenhouse Gas Protocol, this is the primary basis for Greenhouse Gas Accounting. It’s a standard (several in fact) that defines how you translate the activities of a business into a greenhouse gas emissions output. The accounting practices that are applied involve several different steps to translate activities such as electricity used, waste disposed of or miles driven (fuel consumed), into an emissions value.

The Carbon Currency

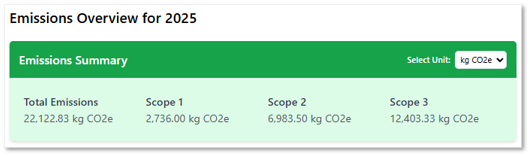

We generally talk of a Carbon Dioxide Equivalent value and the shorthand for this is CO2e. Our platform uses kg CO2e as the default measure, you can select tonnes too. This is the default accounting measure across carbon accounting practice. In financial accounting you might have a default of USD, GBP or EUR depending on where you’re operating from or reporting to.

The ‘e’ in the CO2e stands for ‘equivalent’ and the measure is calculating the equivalent CO2 of all the seven greenhouse gases agreed as needing addressing when the Kyoto Protocol was put in place in 1992, collectively referred to as the “Kyoto basket.” These gases are carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), sulphur hexafluoride (SF6) and nitrogen trifluoride (NF3).

Each gas is weighted by its Global Warming Potential and aggregated to give total greenhouse gas emissions in CO2 equivalents. For example, the CO2 equivalent (CO2e) of 1 kg of nitrous oxide (N2O) is approximately 298 kg of CO2. If you know you emitted 1 kg of N20 then your Carbon Ledger, being standardised to show CO2e, would show a value of 298 kg CO2e.

This of this like converting your commercial activity conducted in JPY, EUR, CAD, USD, etc. to your preferred currency such as GBP.

Accounting Principles

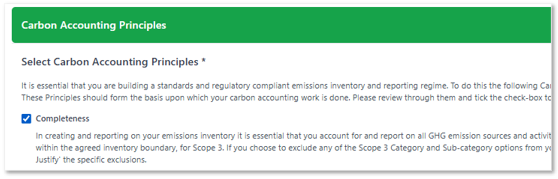

The GHG Protocol is principle based and states that all carbon accounting must be done in alignment with the following principles (think GAAP and IFRS for finance):

- Completeness, Accuracy, Transparency, Consistency, Relevance

When you set-up on the Platform you’ll be guided through these principles and given a clear contextual description of each. Later on you can review them through the Settings menu. They’re also pulled forward into your Interim and Annual Carbon Accounting Reports.

Fundamental Principles and Methodologies

The foundational building block of Carbon Accounting of Scope 1, 2 and 3 we’ve stated before, but here’s a reminder:

- Scope 1 – you own and control the asset and are using energy directly (e.g. gas, oil). Good examples are those back-up diesel generators on AI data centres, the petrol powered mowers for that landscaping business or the gas powered patio heaters at your restaurant outdoor garden.

- Scope 2 – this is consumption of energy (e.g. electricity, gas) provided by a third party. You don’t own or control the asset generating the power but you do consume the output. The emissions from this consumed power are the power company’s Scope 1 direct emissions, but your Scope 2 indirect emissions.^

- Scope 3 – This is everything that supports your business operations but that are outside of your control. Things like business travel and commuting on trains, planes and buses. The disposal of waste and end of live treatment of products you create.

With this understood we move onto a methodological hierarchy of ensuring data quality based on a sliding scale of comprehensiveness and completeness. In an ideal situation we would always want to have high quality primary data that is entirely accurate in terms of emissions values, however that ideal situation rarely exists, so we end up falling back on a hierarchy of primary, secondary and tertiary data.

- Primary level data – supplier reported data, the supplier tells you the exact kg CO2e emissions that resulted in the product they are providing.

- Secondary level data^ – not direct from the supplier but data reported publicly for emissions of similar products and services in a similar region, industry or service with essentially local or national constraints.

- Tertiary level data – also referred to as proxy data as the CO2e value is derived, not calculated. There are two ways to acquire this approximated emissions value; the Average Data Method which is an industry wide average of emissions intensity and Spend Based calculations.

Where most companies start is usually a mix of Primary supplier reported and Tertiary Spend Based, as companies are usually very good at tracking spend and why it’s the Office Manager, Procurement Team or Accounts team member that we see most often getting involved at the start of a company’s journey. Later on the messy middle gets resolved to bring in that ‘comprehensiveness and completeness’ we spoke of earlier.

Accounting for Environmental or Impact Materiality

Materiality looks at how a company’s operations affect the environment, regardless of financial consequences. This is especially relevant for stakeholders interested in sustainability outcomes. Ultimately the impact on the business, the marketplace and the organisational revenue is the point of Carbon Accounting, meaning materiality is critical.

Let’s give a concrete example. The materiality of these seven greenhouse gases become particularly relevant when you’re company uses a certain gas in its operations – in refrigeration or any other form of cooling for example. You’ll need to capture ‘fugitive emissions’ of specific gases from equipment, plant or machinery that use them. How will you know what types and volumes? It comes back to the basics of good record keeping in your financial accounts (Purchase Orders, Invoices), clear processes in your operations (Delivery Notes, Maintenance Schedules) and understanding that carbon accounting, like financial accounting, is affected by and affecting the whole business.

That’s why in our consultative approach we provide Finance, Resource & Audit (FRA) and Governance, Transformation and Strategic Planning (GTS) services alongside Carbon Accounting. They’re inseparable.

Materiality is not just a negative to address, as was mentioned when I spoke to Aszadur Rahaman a while ago regarding data centres and IT operations decarbonisation and more recently Neil Trivedi with regards to sustainability in manufacturing – materiality identified through carbon accounting provides incredible opportunities to improve the revenue of the company by looking at process, practice, materials, supply and waste. Just like good financial accounting does

VC

Chat with us about all things Carbon Accounting – book a free 30 minute call

Footnotes

^ The financial accountants amongst you will no doubt be sensing a double accounting issue here. Double counting across Scope 1 and Scope 2 is OK – it’s not about avoiding double accounting like in financial accounting. This is about accounting for responsibility for emissions.

^^ Depending on who you read or listen to the Secondary Level Data stated above is still Primary Data. We have argued before this makes no sense as it is not drawn from a ‘primary’ source but (usually, depending on format) primary source data collated to generate a localised average. A calculated average is not a primary source, it is a secondary source. A Wikipedia article is a secondary source. The sources of information for the Wikipedia article are primary sources. To think otherwise is to develop unclear models, an issue we’ve seen numerous times.